The month of March often marks the change of seasons from winter to spring. “In like a lion, out like a lamb,” the old adage goes. It’s a time of renewal for the planet we live on. Rays of sun warm a cold landscape, nascent leaves bud in the trees, vivid flowers bloom from the dull ground. It’s a beautiful time of year. It always reminds me of the fact that life is an amazing combination of both progress and recurrence. Progress because we’re getting older. Recurrence because once again we’re experiencing the same turning of the seasons we’ve known since we were children.

Securities markets have the same dual nature. In the long run there’s ongoing growth, but there are also short-run cycles that repeat themselves. Unfortunately, these cycles are not always as predictable and pleasant as the change of seasons! Certainly, the six-week drubbing that began the year for equities was not enjoyable to most investors.

Looking Back

Interestingly, it was only ten days after Punxsutawney Phil claimed an early end to winter that the market bottomed. Since then the S&P 500 has gained over 11%. Far be it from me to recommend that anyone allocate scarce monetary resources based on the whims of a large rodent, or the length of women’s skirts or what team wins the Super Bowl (all of which have been said to predict the stock market). Serious investors must not confuse association with causation. But it’s very interesting to note that folklore can in some cases provide better guidance to investors than even the best-laid plans that are emotionally abandoned after an unexpected decline. Maybe there’s some logic to the old folklore after all!

In its first quarter Market Know How publication, Goldman Sachs made an excellent observation in this regard: “Amid the rocky start to 2016, we believe investors should appreciate the statistical inevitability of market corrections and drawdowns. While it would be a grave mistake to dismiss the risk of reflexivity, since 1990 the equity markets have enjoyed 21 positive calendar years. Of those 21 years, 19 tested investor resolve, with annual lows averaging -5%.”

In other words, investing in equities requires patience. Investable fundamentals tend to change slowly, while market sentiment can change very abruptly. You have to tolerate the recurrent periods of decline to enjoy the long-term growth. That is why it’s important that every investor have an asset allocation strategy that suits their risk tolerance, and won’t be abandoned when the inevitable test of resolve comes.

My last newsletter was written while we were in the throes of the decline, surrounded by a soft patch of domestic economic data (especially in the manufacturing sector). Fears were mounting that the decline in oil prices might be signaling weaker global growth, rather than simply a supply-side shock. Some worried the U.S. economy would veer into recession from a too-aggressive Federal Reserve and weakening Chinese growth. Into this environment, I injected a somewhat light-hearted analogy of jumping sheep to illustrate the gap between market performance (very poor) and fundamental economic conditions (mixed, but not too bad). This was not to dismiss the concerns of the market, just the magnitude of the reaction. At the end of the year we may well look back on the whole thing as a classic example of sentiment getting ahead of data. It’s hardly an uncommon event, especially in the initial stages of a Fed rate hike cycle such as we are in.

Reinforcing this view, here’s what has happened since the market-low on February 11:

S&P 500 Index +11%

MSCI Emerging Markets Index +13.6%

(ICE) Brent Crude + 33% ($40.14 vs. $30.06)

10 Year Treasury Yield + .33% (1.97% vs. 1.64%)

S&P GSCI Commodity-Indexed Trust +15.6% ($14.10 vs. $12.20)

But even if the early year correction was more of a “mis-correction” driven by sentiment, a question remains: What has caused the more recent rebound? Some of the main drivers appear to be:

- Stabilizing oil and commodity prices

- Modestly improving views of the U.S. economy

- Lower banking reserve requirements in China (along with assurances of a more stable currency policy)

- Bigger than expected actions taken by the European Central Bank (ECB) to lower interest rates and broaden its bond purchase program

The upshot is that things look and feel brighter now than they did in the dead of winter. But there is still a lot of 2016 to come.

Looking Ahead

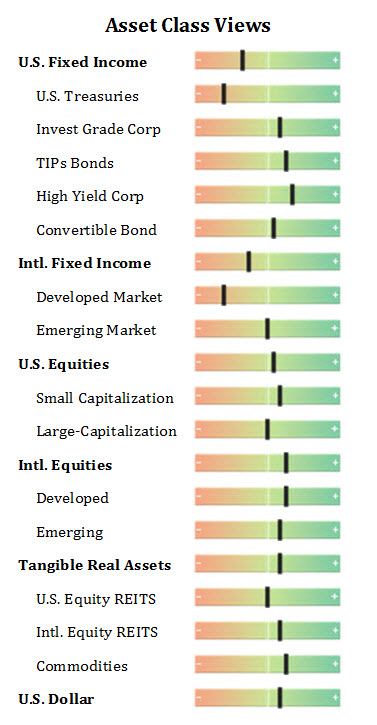

Commodity prices seem to be in the process of finding a bottom. This has been fueling global stock gains since mid-February. It has especially benefited energy and mining stocks and the currencies of countries that are net exporters of commodities. It has also aided a strong rebound in high-yield bonds in general, and those in the commodity and energy space particularly. As more evidence develops that commodities have indeed stabilized, deflationary fears should recede. This should prove beneficial to risk assets going forward. But these same forces may also exert upward pressure on Treasury yields, which should benefit investment-grade and high-yield credit over Treasury bonds.

As with commodities generally, oil prices appear to have stabilized. Signs include the following:

- The number of rigs drilling for oil and gas have fallen to the lowest level since at least 1940, according to oil services company Baker Hughes.

- U.S. oil production is expected to drop steeply in the coming months, from some 9 million barrels-per-day to about 8.5 million, according to the International Energy Agency (IEA).

- About 15 (depending who does and doesn’t show) OPEC and major non-OPEC producers, accounting for some 73 percent of global oil output, plan to hold talks on April 17th in Doha on an initiative to freeze production. If they are successful, it would be the first such global supply deal in over 15 years.

For now, this is all good news for the energy sector. It takes pressure off of margins and improves the outlook for energy-related stocks and bonds, which have weighed on the broader market this year. But looking at the not-too-distant future, it also brings the possibility of unpleasant surprises to the upside in oil markets (wouldn’t that feel strange!).

In their March 16 meeting, Federal Reserve officials struck a more dovish tone than they had at the end of 2015, holding interest rates steady and projecting two quarter-point hikes by year-end. They expect moderate economic growth and strong job gains will allow them to keep to this path. But they also noted that risks to their outlook could come from soft global growth and market volatility. The U.S. dollar dropped on this news, especially against currencies like the Aussie and Canadian Dollar. Emerging market currencies have been strengthening against the dollar as well.

Worth noting, on the same day the Fed made its announcement, U.S. core inflation (ex. Energy and food) increased more than expected, to 2.3% for February. Mounting domestic price pressures are becoming more evident as rent, medical and apparel costs rise. Firmer commodity prices, a softer dollar and improving employment may continue to pressure inflation in the coming months and force Fed officials to adopt a less dovish tone. But for now, these developments are favorable to equities, as they serve to diminish deflationary fears. Any firming of economic growth from here should especially favor value stocks, which have some catching up to do, as well as Treasury Inflation Protected Securities.

European stocks should benefit from the tailwinds of the European Central Bank’s decision to step up its quantitative easing (QE) program. In fact, they are likely to have more upside in this environment than U.S. stocks. I also like European real estate markets, which remain well below past peaks, and which the new QE should benefit.

Conclusion

Having looked ahead at the coming year, I am reminded how much I love spring. Sometimes I think if it could be this season all year long I would be a very happy camper. But then I realize God’s plan is better. Seasons come and go like old friends. Each new season brings memories of those past and the promise of more to come. We can’t stop them any more than we can stop time. It’s the same way with financial markets. We can’t always experience the thrill of running with the bulls. But if we stick with well-laid plans, in the fullness of time we can hope to reap a very bountiful reward! Thank you for reading and if you happen to be a client, thank you for your business!

Disclosures: The views expressed are those of Byron Green as of March 17, 2016 and are subject to change. The information contained herein does not constitute investment advice or take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Additionally, this publication is not intended as an endorsement of any specific investment. Investing involves risk and you may incur a profit or a loss. Information contained herein is derived from proprietary and non-proprietary sources. We encourage you to consult with your tax or financial advisor. Click here to read the GIM Form ADV Part 2 for a complete list of Green Investment Management’s services.

![]() Click here to download printable PDF of GIM Market Commentary 03-17-2016

Click here to download printable PDF of GIM Market Commentary 03-17-2016