Slowing growth in China, swings in oil prices, declining commodities, widening credit spreads and a Fed that is trying to normalize interest rates are all contributing to a risk-off environment and a rocky start to the New Year for investors. While these concerns are carryovers from last year, they seem to have intensified of late as broader concern about global growth has taken hold.

China was the first catalyst for market turmoil. The yuan devaluation last August appeared to be implicit proof of a slowdown in the world’s second largest economy. The market’s reaction then led to ineffective efforts by the Chinese authorities to control the volatility. This led to still greater concerns about the ability of Chinese leaders to provide an appropriate response that supports both the markets and the economy.

Next, equities became increasingly correlated with energy. Many investors came to see declining oil prices as a canary-in-the-coal-mine for global economic weakness. Data actually suggests that elevated inventories are due to excess production rather than too little demand. But that hasn’t quelled investor anxiety or stopped corporate credit spreads from widening, even in sectors outside of the commodity complex that should stand to benefit from lower prices.

Combined with oil concerns, the U.S. economy, long the stalwart in the global economy, has produced some troubling data in manufacturing, trucking and rail volumes. Investors have grown accustomed to viewing the U.S. as the steady engine of global growth, so this has shaken their confidence. As typically happens, investors appear to be overreacting to their fears instead of making a careful evaluation.

Not to dismiss market worries, but their magnitude may be excessive. Even minor inflections to growth seem to be raising fears of a repeat of the Great Recession. While that event may be on investors’ minds, it does not mean that conditions now are the same as then, when it looked like the entire financial system might freeze-up. But a crisis of confidence can always create a self-reinforcing feedback loop in which declines lead to declines.

It reminds me of an interesting incident I read about several years back. In the small Turkish village of Gevas, local shepherds left their sheep to graze on a mountainside while they had breakfast. It wasn’t long before one sheep from the flock of nearly 1,500 stepped too close to a nearby cliff and plunged to its death. Before the astonished shepherds could respond, the rest of the flock followed the first one over the edge. Fortunately, not all of the sheep died. The first 450 that perished cushioned the fall for those remaining!

There have been similar reports of ‘jumping sheep’ incidents in other places. Why do they do this? It seems that a sheep’s only true defense from danger is to stay in the flock in hopes of avoiding being culled by an impending threat, be it wolf or cliff. Don’t get me wrong. Most investors have much better intellects than do sheep! But they sometimes overreact to situations without a clear picture of the risks involved. It can be safer to ignore the herd. The current risk aversion, in my view, is creating significant opportunities. That said, the volatility at present calls for disciplined risk management, analysis and patience in executing a strategy.

To get more specific, below is my view of some of the key sources of fear in the market. After that I will address the opportunities.

- What is happening in China today is a continuation of efforts began almost six years ago to rebalance their economy from export and investment-led to consumer-led. It has been a slow and uneven process, but one that should ultimately benefit China and the global economy. To get this transition moving along more smoothly, the market needs to see China get its policy responses correct regarding equity markets, interest rates and currency valuation. In the meantime, I don’t see China being pushed into a disruptive depreciation of the yuan, given its current account surplus and foreign exchange reserves. I expect they will continue to expend foreign currency reserves to keep their currency stable and improve their credibility – especially since their currency was just approved by the International Monetary Fund (IMF) as a global reserve currency last November. The yuan will be officially added to the IMF’s Special Drawing Rights (SDR) basket of currencies on October 1, 2016.

- The manufacturing and industrial parts of the U.S. economy that are linked to trade have clearly been going through a recession for months now as they try to adjust to oil and commodity prices, cutbacks in capital spending and a stronger dollar. However, the relatively healthy and much larger consumer-led side of the economy is growing at a respectable rate. U.S. retail sales for January showed solid growth of 3.4% over January 2015. This seems to be helping allay U.S. growth fears for now. And combined with continued solid jobs growth in January, it seems unlikely that the current industrial downturn will lead to a general recession in the near future. In fact, the retail sales data immediately led numerous investment firms to raise their first quarter estimates for U.S. growth.

- To dispel concern that the corporate high yield bond market’s exposure to the energy and commodity sectors is akin to the subprime mortgage meltdown in 2006, consider a quote from Deutsche Bank AG Chief International Economist Torsten Slok. In a February 1, 2016 article titled If You Think the U.S. is in Recession, Start Buying Stocks Now, Slok pointed out that “the high yield problems today are 15 times smaller than the housing market imbalances we were facing in 2006.” He also noted that all high yield bond debt outstanding represents only 2% of total U.S. debt today, compared to 30% in the case of mortgage debt in 2006. The banking system is also far less leveraged today, and much better capitalized.

- With its first increase in rates behind it, the Federal Reserve’s tightening cycle has begun. But expectations for more hikes are being revised lower by experts. A slower and more gradual liftoff appears likely. This should help ease anxieties about the potential impact to the markets.

- Historically, recessions have not been foreshadowed by falling oil prices. And the energy sector is already in the process of rebalancing supply and demand. Low oil prices have supported demand growth at the fastest rate in a decade, and U.S. supply has begun to trend lower. According to the International Energy Agency (IEA), global supply dropped 0.2 million barrels a day (b/d) to 96.5 million b/d in January, as higher OPEC output only partly offset lower non-OPEC production. For 2016 as a whole, non-OPEC output is expected to decline by 0.6 million b/d, to 57.1 million b/d. Overall in 2016, demand should grow by 1.2 million b/d over the course of the year. Additional supply from Iran as sanctions are lifted is not likely to keep up with demand. If the data from the IEA is correct, the market may move from excess inventories to a more balanced state or even a deficit as we reach the latter part of 2016. In addition, Saudi Arabia and Russia held talks in the Qatari capitol of Doha Tuesday in which they agreed to freeze output levels. Further agreements could happen.

As to opportunities, coming into 2016 I had modest return expectations for equities. Nonetheless, I have been surprised by the scale and speed of recent declines. But as Benjamin Graham, the father of value investing, once said, “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” This dual nature can be a good thing. It provides opportunities to pick up real value. That’s why Jamie Dimon, the CEO of JP Morgan, bought 500,000 shares of his company’s stock after it had fallen around 20% since the first of the year. He has bought 500,000 shares twice before in the last 12 years, in January 2009 and July 2012. They were both very opportune purchases.

In developed markets outside the U.S., I expect that economic growth should firm up as the year unfolds, especially as policy is likely to turn more accommodative in Europe and Japan. In emerging markets, Brazil and Russia should improve from their deep contractions of 2015, while India and Mexico should experience more rapid growth. China will likely remain on its bumpy path toward a slower but more balanced growth trajectory.

The greatest risks outside the U.S. appear to be related to China’s growth, as well as in the commodity focused export economies. Unless there is a new fall in growth rates or commodity prices ahead, a great deal of that risk has already been factored into market levels.

Overall, we need to be prepared for volatility as the year progresses, but the reset we have experienced since last summer has uncovered opportunities in several areas. Let’s take a look at those now.

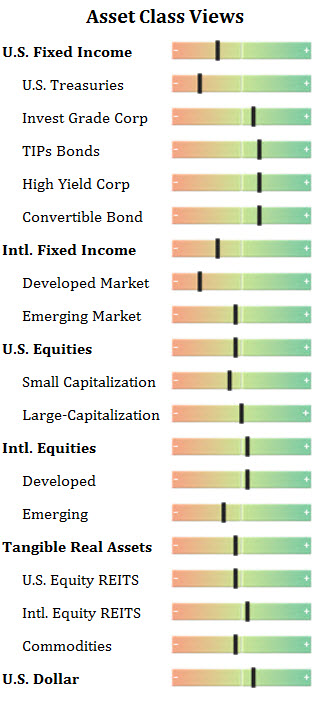

One of the emerging opportunities is in the credit space. This is surprising since the current bond environment is marked by ‘fixed loss’ investing, with investors on a global scale buying sovereign bonds with negative interest rates. Did you ever think you would see individual investors and institutions willing to earn negative rates, a guaranteed loss? The only way you can make money with these bonds is to expect that you can pawn them off later at a higher price with a still more negative potential outcome for the new buyer.

In U.S. corporate bonds, especially among high yields, there is a different opportunity developing. Total returns to the BofA Merrill Lynch High Yield Master II Index (MLHY) have been flat to negative for almost three years as declining oil and commodities have taken their toll on bonds in these industries. Moody’s has forecast that speculative-grade defaults in general will rise to 4.4% in the U.S. in 2016, and stay near 3% in Europe. Default rates in the resource industries could climb even higher. But the market has priced this in, and yields for the MLHY have risen to 9.9%. And if you exclude bonds from the higher risk industries that represent approximately 12.4% of the index, you will find that bonds from other industries have been made guilty by association. They are trading at elevated yields with discounted prices. This is an increasingly attractive opportunity. Current yield spreads over Treasuries are at 7-year highs of 8.6% for the MLHY. As the end game for a balancing of oil supply and demand comes to fruition, I see the potential for attractive total returns from high current yields coupled with price appreciation as credit spreads narrow.

Another more conservative, yet still attractive opportunity is in Treasury Inflation-Protected Securities (TIPS) as a substitute for nominal Treasuries. The spread between the two, a measure of inflation expectations, should widen in favor of TIPS as the year progresses. Spreads for 5-year TIPS currently imply a 1.09% inflation rate, reflecting the markets’ deflationary fears. If these fears subside, the market should price in higher rates of inflation. And if oil prices rebound at all, it could drive additional performance from TIPS over nominal Treasuries.

In equities, opportunities will be driven largely by improvements in earnings and risk appetite. The S&P 500 is priced at approximately 15.3 times 12-month forward earnings estimates of $124.25, according to FactSet Research. This is approximately a 4% rise in earnings over last year. Dividends in the index rose by approximately 10% last year. This year, look for the bigger opportunities for appreciation to come from the developed markets of Europe and Japan. Mario Draghi has said the European Central Bank (ECB) will review and possibly recalibrate policies at its next meeting on March 10. This is a strong indication that more easing is on the way. With the Federal Reserve in a tightening phase, continued easing from the ECB and the Bank of Japan should contribute to continued low global rates and a stronger dollar. Those factors should accrue to the benefit of both Europe and Japan.

In conclusion, the markets have reacted harshly over recent months to growth fears that are being driven by many factors, including U.S. interest rate hikes. History tells us this is a relatively common occurrence. A recent study from Phillip Miller of Strategic International Securities, Inc. pointed out that there have been 15 non-recession corrections of 9% or more in the S&P 500 since 1970. Of those, 12 were associated with rate hikes. Only one exceeded 20%, and that was the decline in 1987. The S&P 500 actually ended that year slightly higher than it began. Today, the S&P 500 is down about 14% from its May 2015 highs. Absent a recession, the brunt of the decline may be behind us.

Those are my views for now. Thank you for reading, and thank you especially for your business.

Disclosures: The views expressed are those of Byron Green as of February 17, 2016 and are subject to change. The information contained herein does not constitute investment advice or take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Additionally, this publication is not intended as an endorsement of any specific investment. Investing involves risk and you may incur a profit or a loss. Information contained herein is derived from proprietary and non-proprietary sources. We encourage you to consult with your tax or financial advisor. Click here to read the GIM Form ADV Part 2 for a complete list of Green Investment Management’s services.

![]() Click here to download printable PDF of GIM Market Commentary 02-17-2016

Click here to download printable PDF of GIM Market Commentary 02-17-2016